Importance Of AI-Driven Fraud Detection and Prevention Systems In The Financial Ecosystem

In the last three years, AI-driven fraud detection and prevention has become increasingly prevalent in the financial ecosystem.

A high total of thirty-three thousand, six hundred and forty-one (33,641) cases of fraudulent activities were reported in the second quarter alone of 2021 (NIBBS second quarter fraud report,2021).

Although there has been a 43.41% decrease in reported fraud cases recorded from the first quarter, the number of these reported cases is staggering high costing the financial industry a loss of over ₦594.18 million in the second quarter of 2021 (NIBBS second quarter fraud report,2021).

The volume of successful fraud attempts carried out has increased by 4x between the periods 2019 and 2021 (StearsBusiness, March 2022).

With such high volumes of successful fraud attempts and losses, one is moved to query how these fraudsters achieve such success rates and which channels.

Between the period 2020 to date, fraud value lost through financial channels increased from ₦5.04 billion recorded for the first nine months of 2020 to ₦7 billion in the same period of 2021 — a 34% increase (StearsBusiness, March 2022).

The most common fraud channels as of Quarter 2 of 2021 recorded according to fraud volume have been

- Web channel applications

- Fraudulent Withdrawals (in bank branches & clearing cheques)

- Mobile application

- ATM

- Point of Sale (POS) Terminals

Web channels alone accounted for a loss of ₦4.52 billion, ranking first among the channels, Fraudulent Withdrawals accounted for a loss of ₦815.6 million (Nibbs second quarter fraud report,2021).

See the chart below for a complete analysis:

With all these huge financial losses going on through these channels does it mean the financial organizations do not have controls put in place to mitigate and prevent such losses to fraud?

The answer to that is NO!

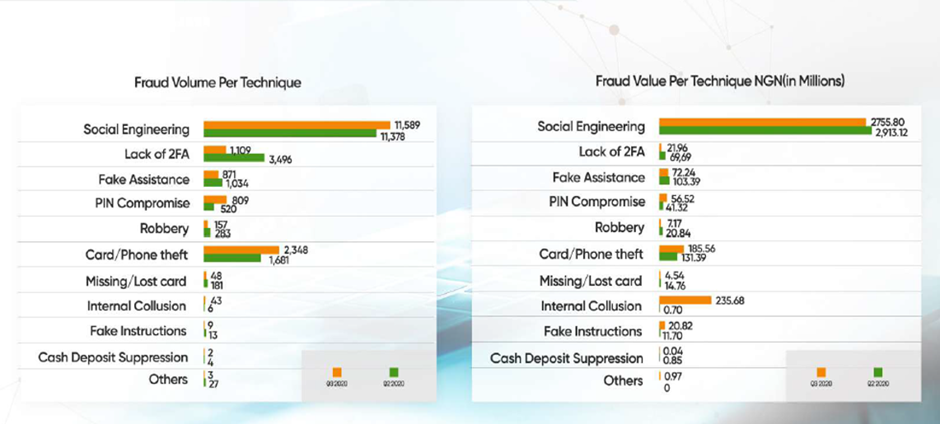

This means that these fraudsters have devised Several techniques, from card theft to PIN compromise, to aid in carrying out their activities thereby beating the controls put in place. However, social engineering, which involves manipulating people to give out sensitive information, is the most common and arguably most dangerous technique.

In 2020 social engineering accounted for a fraud loss of over ₦4 million, becoming by far the most successful fraud technique used by fraudsters. View the chart below:

An artificial Intelligence-driven anti-fraud system is a potential solution, but it comes with challenges ranging from cost, limited resources, talent shortage, and lack of systems. As a result, only 25% of the institutions surveyed by PwC are using artificial intelligence (StearsBusiness, March 2022).

A recommendation of several layers of security would be advised as best for financial institutions.

They could first protect their systems by protecting their customers, AI intelligent systems are out there that study customer behavioural and transactional patterns and come up with intelligent predictive model sets, that would flag a user as fraudulent if and when they deviate from the model.

An advanced fraud system can be a second layer to monitor transactions and detect fraud attempts such as Anti-Money Laundering, card fraud, and cross-bank fraud.

It is therefore imperative that a mechanism be put in place to not only identify fraudulent activities as they occur but also build a system that can predict such events before they happen.

Implementation of the GRC concepts can serve as internal controls to identify early potential fraud risks internally and mitigate these risks as such,

Are you interested in leveraging an agile GRC platform to establish and measure compliance best practices while managing and responding to risk to protect your business? Give us a call today or visit ActivEdge Website to learn more.